Key challenges ahead for new Federal Reserve leadership

Review the latest Weekly Headings by CIO Larry Adam.

Key takeaways:

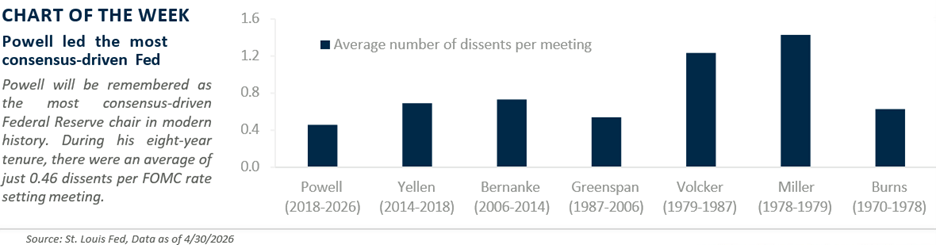

- Powell will be remembered as the most consensus-driven Fed chair

- Warsh inherits a Fed that has missed its inflation target for over five years

- Warsh likely to be tested on his inflation resolve and political independence

Leadership transitions at the Federal Reserve (Fed) are rare. Only seven individuals have served as Fed chair since the 1970s, underscoring how infrequent turnover is at the Fed’s top job. That rarity is why investors pay close attention when a new chair is appointed, especially when the incoming leader brings a different perspective. Kevin Warsh has been a vocal critic of Fed policy and communication in recent years. With his official confirmation by the Senate to succeed Chair Jerome Powell – an outcome that appeared uncertain just weeks ago – the Fed is entering a new era. This transition raises important questions about the future of monetary policy and the challenges ahead as markets adjust to new leadership. Below, we review Powell’s legacy and his steady guidance through unprecedented times and outline key challenges Warsh will face as he takes the helm.

Looking back on Powell’s legacy

Jerome Powell served two full terms (2018–2026) as Fed chair, guiding the economy successfully through extraordinary shocks, including a once-in-a-generation pandemic, two geopolitical conflicts that drove energy price spikes, a regional banking crisis, and a reshaping of global trade that pushed tariffs to their highest levels since the 1940s. In the final stretch of his tenure, Powell also faced intense political pressure and will break with historical precedent by remaining on the Federal Reserve Board after stepping down as chair, the first such instance in 80 years. Despite these challenges, Powell will likely be remembered for his steady, consensus-driven leadership, marked by the lowest average dissents per meeting of any Fed chair. While his post‑pandemic “transitory” inflation call remains a notable blemish, Powell’s legacy will ultimately be defined by his steadfast defense of Fed independence.

Three near-term challenges for Warsh

With Powell’s term ending, Kevin Warsh starts as the next Fed chair today. As an outspoken critic of the Fed, he brings an ambitious reform agenda, including shrinking the Fed’s balance sheet, curbing reliance on non-traditional monetary policy tools like Quantitative Easing, streamlining communications, and reassessing inflation metrics and legacy models. However, he is stepping in at a particularly challenging moment. Right out of the gate, Warsh’s immediate tests will include:

- Tackling rising inflation: Warsh inherits a Fed that has overshot its inflation target for more than five years and now price pressures are reaccelerating. Between last year’s tariff shock and renewed energy price spikes tied to Middle East tensions, headline inflation has climbed to a three‑year high of 3.8%. Recent data have been somewhat distorted – held down by collection issues during last year’s government shutdown and temporarily lifted by higher gasoline prices – but the underlying trend remains firm. In fact, the three‑month annualized pace is now running over 7%, pointing to potentially more persistent inflation pressures. With the broader economy still resilient – supported by tax refunds, lower corporate taxes, and an AI‑driven capex boom – the risk of entrenched inflation is rising. Getting ahead of it will be one of Warsh’s most immediate and critical tests.

- A deeply fractured Fed: Warsh will assume leadership of an increasingly divided Federal Reserve, complicating his efforts to forge consensus on rate decisions and alignment around a new policy framework. Case in point: At the April Federal Open Market Committee (FOMC) meeting, four members dissented – with one voting for a rate cut and three opposing statement language that signaled an easing bias – highlighting meaningful internal disagreement. Adding to the challenge, Powell’s decision to remain on the Board of Governors introduces an unusual dynamic. While Powell plans to maintain a “low profile” and has no intent to act as a “shadow Fed chair,” his continued presence may still complicate Warsh’s efforts to consolidate authority, build support and avoid the perception of a dual power dynamic within the Fed.

- Pressure to cut rates: Warsh will face an early test of Fed independence as he navigates persistent White House pressure to lower interest rates. While he has argued that AI‑driven productivity gains could help cool inflation over time, it may be a tough sell to the broader FOMC while inflation remains elevated due to Iran‑related energy price shocks. At the same time, Warsh may need to rein in more hawkish voices on the committee that could favor signaling a tighter stance as inflation pressures build and stimulus from the One Big Beautiful Bill and AI‑related investment cushions economic risks. The key question is how long Warsh’s honeymoon period lasts before political scrutiny ramps up, especially with midterm elections approaching.

Bottom line

As Warsh prepares to take the helm at the Fed, how he navigates these crosscurrents will define the early days of his tenure. Markets are quick to test new Fed chairs and Warsh will likely need to prove both his resolve to contain inflation and his independence from White House pressure. That tension could fuel added volatility in the months ahead, especially as investors assess proposed policy shifts that may face internal resistance at the Fed. Still, we expect near‑term inflation pressures to ease in the second half of 2026, allowing the Fed to cut rates once by year end or early 2027.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success.

Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

The S&P 500 Total Return Index: The index is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 7.8 trillion benchmarked to the index, with index assets comprising approximately USD 2.2 trillion of this total. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization.

Sector investments are companies focused on a specific economic sector and are presented here for illustrative purposes only. Sectors, including technology, are subject to varying levels of competition, economic sensitivity, and political and regulatory risks. Investing in any individual sector involves limited diversification.